How do I get rich?

A very short introduction to managing your finances.

Money is power. It enables us to live life on our own terms and make the world a better place. Yet women are remarkably reluctant to take control of their finances.

Almost half of millennial women defer to their spouses for financial decisions, according to a UBS survey

Women are still on the back foot when it comes to money. Our salaries are lower than men’s and our wealth is significantly smaller. By some estimates for every dollar a white man owns, women overall own just 32 cents (US numbers)!

Women also receive significantly lower pensions. European women’s pensions are about 28% lower than men’s. Consequently, women in the Western world are about 30% more likely to be poor than men.

But change is in the air. Young women are starting to leave men behind. In the UK, 21- 16-year-old females now outearn their male peers. For the first time in history, more women graduate from university than men.

Women are getting richer. They control about a third of global wealth and add $5 trillion to the wealth pool globally every year. This is outpacing the growth of the wealth market overall.

Things are moving in the right direction but there is more we can do to put our hard-earned cash to work.

Pillar One: Take control

There are three pillars to managing money and optimising finances: work, investments and spending. To live a rich life, it’s necessary to look at all three.

The first step should always be to take stock and look at your outgoings, savings and investments. The next step is to set a budget.

Analyse your spending. Add up what your fixed payments such as rent, groceries, transport, bills and optional payments such as holidays and leisure are.

Set a budget. You could use the rule of thirds or the 50/30/20 rule: 50% goes to needs, 30% goes to wants, and 20% goes to savings & investments. Sometimes this is not realistic but you should at a minimum save and invest 10% of your net income.

Evaluate your outgoings and make sure regular payments such as gym memberships, mobile phone contracts and subscriptions are value for money and that you actually use the services.

Set priorities for spending on optional activities. Cut down on things you don’t need and critically evaluate what brings you happiness.

Make sure you have an emergency fund of at least 3 months of living expenses in an easy-access savings account (paying interest).

If you have debt make a plan on how to pay it off.

Pillar Two: Boost your career

Women get less money out of paid work compared with men. Across Europe and the US women earn about 13% to 17%* less than men per hour. This is called the gender pay gap and is driven by various factors including women working part-time, being over-represented in lower-paid professions, and discrimination at work (gender promotion gap, glass ceiling).

Sadly, as individuals, we don’t have control over some of these issues. Working hard and being smart is not enough. I know that from personal experience. I sat in meeting rooms crying my eyes out for (unfairly) being passed over for promotions and being held to higher standards than my male peers. I had to make some tough decisions to advance my career.

Because we face additional hurdles, it is important to take control where we can. Advocate for yourself and other women whenever there is an opportunity:

Ask for pay raises and promotions. Don’t sit around waiting for someone to give money to you.

Stay on the lookout for career opportunities and be brave enough to take them when they arise.

Network wherever you are. Tell people about your skills and your goals. You never know where this leads to.

Be confident! (Numerous studies show that men consistently overestimate their intelligence & abilities and women underestimate theirs).

Support other women in the workplace. Call out poor behaviour and challenge discrimination.

Be mindful of the effects of children on your career and finances. The biggest factor negatively impacting female lifetime earnings is the so-called motherhood penalty.

In the rich world, 80% of the gap between male and female labour force participation is explained by women dropping out after the birth of their first child. Looking after children is important and rewarding work but sadly we live in a world that doesn’t respect this choice and consequently becoming a stay-at-home mother puts women at a profound and lasting disadvantage.

That’s why we should all aim to have children with a man who is a real partner and willing to do his share of the care work. If you and your partner can’t or don’t want to equally share childcare, you need to come up with a plan that will compensate you financially for reducing or giving up work.

Pillar Three: Investing

Women are more hesitant to invest compared with men. 48% of American women currently have money sitting in investments within the stock market, compared to 66% of men. In Europe it’s significantly worse: 29% of women are investing compared with 47% of men.

This is a problem because investing is the only way to protect your savings from inflation and grow your wealth.

Most of us underestimate the impact of inflation, so let’s look at an example. If we assume an average inflation rate of 3% per year over 5 years this is what would happen to €1,000 in real terms if you do…

(I used this inflation calculator, interest calculator and this mutual fund calculator)

As you can see doing nothing with your money is the skincare equivalent of never using SPF. Inflation will damage your savings (as the sun damages your skin) and you will have to live with the consequences for the rest of your life.

Women often think they don’t know enough about money or the stock market to invest. I totally get that. The language and culture around finance are intimidating. I have worked as a financial journalist for over a decade and even I don’t feel confident at times.

But in reality, investing is less complicated than sophisticated skincare regimes. Studies have shown that women outperform men on average when it comes to investing and spending hours picking the “right” stocks (as many men do) often only achieves underwhelming results. The skincare equivalent would be using 20 products on your skin in the hope that this will prevent wrinkles.

Ready, set, go!

The choice of investments can be overwhelming. You can invest in practically anything that you can buy: luxury watches, real estate and cryptocurrencies are just a few examples. But the most convenient and reliable way remains the good old stock market.

A diversified stock portfolio is a pretty safe bet in the long-term. After 15 years the risk of losing money is tiny, according to Forbes (based on the S&P 500 - a list of the 500 biggest companies on the stock exchange in America).

The MSCI World Index (a collection of global stocks & shares) made an average return of about 11% per year over the last ten years. It’s true that markets you up and down but they always recover. Let’s take a look at the MSCI world through the times:

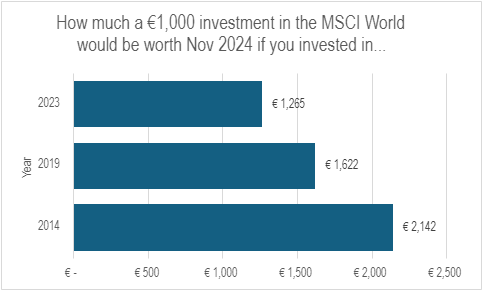

And now let’s take a look at how much money you would have made on Nov. 1, 2024 (before taxes and fees) if you had invested €1,000 on Nov 1 of 2014, 2019 and 2023 using this calculator.

Now imagine what will happen to the money you invest now in 30 years. You’ll be drinking martinis with your old-lady friends while deciding what cruise to go on next (or whatever floats your boat).

How do I get started?

The easiest and cheapest way to start investing is through an online broker and invest in ETFs. ETF stands for exchange-traded fund and they are essentially a basket of stocks copying so-called indexes (a collection of companies traded on stock exchanges).

If you buy an ETF you are investing in a large number of companies at once. A popular choice is an ETF tracking (ie copying) the index MSCI World. The MSCI World index contains about 1,500 global companies. You can check which companies are currently included here.

Follow these steps:

Open an online broker account. I use Scalable but there are many others such as Trade Republic, HL and Trading 212. Don’t overthink it and just pick one.

Start with a small sum that you feel comfortable with. €100-500, for example.

Buy an ETF based on the MSCI World index. I use the Amundi MSCI World V UCITS ETF Acc but there are many others.

You can now either continue investing a small sum every month (as with skincare, consistency is key!) or wait and observe.

Start educating yourself about finance. You don’t need to read boring books or attend webinars. I list some resources including podcasts and a Netflix show below.

Once you feel more comfortable with investing, you can increase the amounts and diversify your portfolio.

A few things to keep in mind:

Stock markets are volatile and go up and down. Don’t panic and just ride out the storm if it crashes. It will recover eventually.

Never invest money in stocks and shares that you need in the short term. Only use the money you plan to keep invested for more than 5 years.

Diversifying your investments lowers your risk significantly. With an ETF based on the MSCI world, you automatically have a high level of diversification.

You should never invest large lumps of money in a single company or a single asset class (Bitcoin or gold, for example).

Stay away from “get rich quick schemes” like day trading (only up to 36% make profits), short selling (can go awfully wrong) and investing large amounts in cryptocurrencies (very volatile). All of these “strategies” come with a high risk of loss. Some of the “get rich quick” products are outright frauds.

You will typically have to pay capital gains tax on the profits you make with your investments. An overview of capital gains taxes in Europe is here. Often the taxes will be collected automatically or you can pay them when you sell your investments and realise the profits. The fees for ETFs are automatically deducted and are usually between 0.1% and 0.4% of the value of your investment per year. Some countries offer tax incentives. Find out about how to use them as this can save you a lot of money.

-*the unadjusted gender pay gap. If adjusted for same number of hours, same qualifications in the same kinds of jobs the gender pay gap is lower but still around 5%.

Recommended Reading, Listening and Watching:

The Savings Expert: “Do Not Buy A House!” Do THIS Instead! - Morgan Housel

Only 18% of Women in Europe Invest, But Times Are Changing | by Janine | ILLUMINATION | Medium

The Confidence Gap - The Atlantic

Please don’t become a stay-at-home mother

Why we have too few women leaders TED Talk

Lean In: Women, Work and the Will to Lead -Sheryl Sandberg

Resources in German

Kostenloser Guide: Investieren an der Börse 2024 von Diana zur Löwen

Finanzen für Frauen einfach erklärt » Finanztipps von herMoney

Finanztip - Deutschlands Geld-Ratgeber

Madame Moneypenny (in German)